Understanding H93: A History of School Choice in Idaho

After years of setbacks and refinements, the Senate voted for Education Freedom last week, and the Governor has signed H93 into law. But the work is not yet done.

House Bill 93, which we passed 20-15 last Wednesday in the Senate and Governor Little signed into law yesterday, has been a long time coming.

H93 and Education Freedom

Low student outcomes and Leftist worldviews imposed in public schools have increasingly highlighted the importance of Education Freedom for many parents. Education Freedom is the right of the People to educate their children as they see fit. This involves the broadening of parents’ options in their children’s education, with a special focus on eliminating governmental restrictions on and suppression of non-public education. H93 advances Education Freedom by expanding School Choice. As exclusive government funding creates a monopolistic environment which suppresses other options (and taxpayers who refuse to send their kids into the failing system are still forced to subsidize it), supporting comparable choices allows market forces to better combat the current monopolistic suppression. While some might argue against any governmental involvement in education, Article IX Section 1 of the Idaho Constitution declares our legislature has the duty “to establish and maintain a general, uniform and thorough system of public, free common schools.” Acknowledging this duty, School Choice is the movement to increase parents’ agency over taxpayer money and resources meant for their children’s education. While this can apply to public school open enrollment policies (Public School Choice) and Charter Schools, the most direct application is the quest to find ways where the Money Follows the Child (Full School Choice).

States all across the nation have a variety of School Choice policies. There are three main ways to empower parents to allocate their children’s education funding. The first is a Voucher Program, a system where parents receive certificates of funding for direct tuition payments to qualifying private schools. The second is Education Savings Accounts (ESAs), where parents are given a savings account to use for certain defined educational purposes. The third is a Refundable Tax Credit, which allows parents of non-public-school students to subtract education-related expenses up to a certain amount from their tax liability, and to be refunded the rest if the credit exceeds what they owe in taxes. This approach is the most streamlined and least bureaucratically-intensive, not inviting as many possibilities of arbitrary governmental restrictions. There is no government-generated list of specific schools or vendors which are or are not eligible for the credit; parents claim the credit for “qualified expenses” defined based on purposes or types of program, not an approved list of organizations. This supports innovative small-scale arrangements such as the use of tutoring services. It also does not require a new bureaucracy to protect against misuse, as serious penalties already exist for tax fraud.

School choice not only empowers parents to seek the paths best for their individual children, but, by harnessing free-market forces, it also is likely to lower costs to taxpayers overall, as competition strengthens the relationship between costs and outcomes everywhere. Per-student costs at private schools are sometimes thousands of dollars less than at public schools, and good school choice proposals cut costs by giving parents less money than is spent per student in the public school system. Furthermore, competition brought by school choice could even raise outcomes at public schools, as some studies suggest. For more research on the effects of school choice policies, check out a summary by Dr. Patrick J. Wolf.

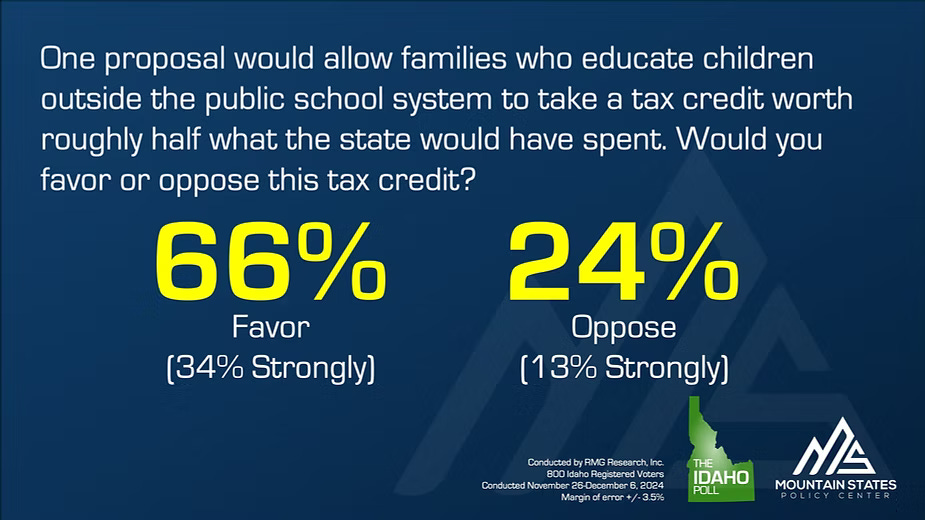

Idahoans Support School Choice

The Mountain States Policy Center, a respected free market research organization, conducts an annual scientific poll on various issues. Their Idaho Poll at the end of 2024 showed strong support for an education choice tax credit.

Notably, this support is broad, including 73% of Republicans, 61% of Independents, and 53% of Democrats. Education reform doesn’t have to be partisan; it’s just common sense.

Timeline of School Choice Proposals in Idaho

There have been many school choice bills which have been introduced and have failed over the years in the State Capitol. The following is a selection of these.

In 1997, the Idaho Legislature considered H342 (1997), which would have granted a tax credit of $500 per student to parents or guardians of school-aged children who did not enroll those children in a public school and were having them educated elsewhere. This bill did not pass. Analyzing it, the AG opined that, while “it is probable that the bill would be upheld as constitutional,” “the constitutionality of HB 342 remains somewhat unclear” in light of questions of possible benefits to religious schools which would potentially violate the Idaho Constitution’s Blaine Amendment.

The next year, recognizing the seriousness of the existing financial burden to parents who pay for their children’s education while also paying taxes to support public education, HCR39 (1998) would have created a committee to study tuition tax credits or deductions for Idaho taxpayers who do not use the public school system. While this resolution passed the House 52-13, it died in Senate State Affairs.

In the spirit of the failed resolution, H686 (2000), which would have created a tax credit for a person or corporation’s donation directly to a parent educating their child outside the public school system, was introduced, but it never made it out of committee. A similar bill, H311 (2001), was introduced the next year, which also added the possibility of parents receiving the credit for their own expenditures. While it passed the House 36-32, it died in Senate Education. These two bills’ statements of purpose imply that the emphasis on parents themselves benefiting rather than schools was “to insure constitutionality” in light of the aforementioned AG’s opinion, concerned that a credit too “dependent upon the payment of tuition” could run afoul of the Blaine Amendment with regard to religious schools.

H76 (2005), another bill with the same concept, died in committee as well. Seven years later, H670 (2012), which was passed out of committee, changed the approach slightly, proposing a credit for donations to official scholarship granting organizations, but it was eventually sent back to committee.

H253 (2019) changed course, advocating for an Education Savings Account program of 90 percent of average per-student funding from the general fund. It died in House Education.

In 2020, the U.S. Supreme Court ruled in Espinoza v. Montana Department of Revenue that the Free Exercise Clause of the First Amendment prohibits religious schools from being specifically excluded from school choice programs, regardless of a state’s Blaine Amendment. Thus, as EdChoice puts it, “Legislators who were once burdened with the fear of hostile and costly litigation with an uncertain result if they adopted school choice programs may now proceed to help their parent constituents by providing educational options for their children.” For a more in-depth analysis of the implications of Supreme Court rulings for school choice in Idaho, check out the February 7 newsletter in my 2023 Session Archive. While this and other rulings laid to rest concerns associated with the 1997 AG opinion, it did not change the atmosphere overnight.

The next year, H294 (2021) tried to combine a $500 grant prioritizing lower income families with a scholarship calculated similarly to the previous ESA, but, after passing the House 47-22, and even when the scholarship portion was removed via amendment, the Senate killed it 16-18.

H822 (2022) then tried to introduce another ESA similar to 2019’s legislation, but it died in House Ways & Means.

S1038 (2023), yet another ESA bill, failed 12-23 in the Senate.

H447 (2024) sought a change of approach from ESAs to a Refundable Tax Credit. This bill specifically emphasized not directing any money from the general fund away from public schools. Even so, the House Revenue and Taxation Committee rejected it 10-7.

After all these setbacks and refinements, the legislature introduced H93 (2025). Similar to last year’s bill, it creates a refundable tax credit of up to $5,000 per eligible student ($7,500 for those with special needs) for parents incurring qualified educational expenses, including tuition, tutoring, standardized test fees, textbooks, and transportation related to nonpublic K-12 education. This is significantly less than the average per-student spending in Idaho public schools (The US Census Bureau estimates Idaho spent $9,670 per student in 2022). The program has a $50 Million cap, and, while generally being first-come-first-serve, provisions include a prioritization for families with incomes up to 300% of the federal poverty level, and a potential for a one-time advance payment in those parents’ first year of participation.

The Idaho Parental Choice Tax Credit is both accountable and non-cumbersome. Transparency is ensured by the State Tax Commission’s administration of the program and annual reporting to the legislature. Unlike much public school education, parents themselves will increase educational accountability by determining what is best for their children. And as already mentioned, tax filing is already a system which severely disincentivizes misrepresentation. Schools also are protected from government overreach by the provision that the bill’s language cannot “permit any government agency to exercise control or supervision over any nonpublic school or to give the state authority to regulate the education of nonpublic school students” and that schools may not be forced to alter their “creed, practices, admissions policy, or curriculum” to accept students whose payment of tuition or fees stems from the credit. As described earlier, a tax credit is the best method of education choice to ensure this protection, as it does not invite a gatekeeping bureaucracy with lists of approved and rejected schools or organizations. In addition to these measures, parents will fill out satisfaction and engagement surveys. This legislation ensures parents have excellent options for their children’s unique educational needs while minimizing government intervention.

For the past few years, some homeschool families have raised objections to school choice legislation, concerned that a credit could come with strings attached and invite regulation of homeschooling. The homeschool movement is diverse, and we have listened to many voices of those concerned about implications for regulation, in addition to those who see the credit as potentially beneficial. I believe we have seriously addressed each of the concerns in drafting the provisions of H93, and we continue to take any concerns and suggestions seriously. I and my wife have homeschooled all of our children, and we are committed to ensuring the autonomy of families in education. This legislation does not force homeschoolers to do anything. One complexity in this process is that, while some homeschool families do not want the ability to be reimbursed for any of their educational expenses, it is difficult to exclude homeschoolers as a group; this could involve narrower definitions infringing on freedom of association and privacy. This issue seems to have materialized in H164 (2025), a competing bill which was rejected; while that proposed credit did exclude homeschool families, it would have subjected parents to an application process involving student testing and other matters, in addition to being administered by the State Department of Education’s regulatory bureaucracy, which might have restricted or shaped the program negatively.

Families do have a right to their own taxpayer money, and I have heard this from many homeschool families. And yet I do agree with some detractors of H93 that a property tax exemption is the most straightforward way to relieve the double burden to homeschoolers from paying both for their own children’s education and the public system. This is why I also introduced S1074, which would exempt families with a school-aged child who do not accept any educational funds from the state (including via use of the public school system) from education-related property tax levies on their primary residences. I will continue to fight for this solution in the future.

The Status of H93 and Future Education Freedom Legislation

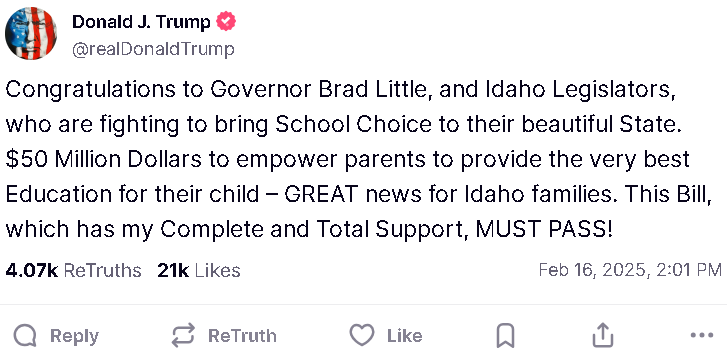

Two weeks ago, President Trump gave H93 his full endorsement, signaling its alignment with his national education freedom agenda.

After passing the House 42-28 and the Senate 20-15, Governor Little signed the bill into law yesterday, bringing the People’s desire for Education Freedom one step closer to fruition.

This landmark victory is cause for celebration, but we will not rest in it. I will continue to advocate for the non-public-school tax exemption, and, first thing next session, I will work to reintroduce HJR1, which fell short of the required two-thirds majority in the House by a single vote. Our current position of strength does not provide an excuse to stop being vigilant; it is instead the perfect time to insist on enshrining fundamental education freedom in our State Constitution, as a heritage to future generations. Let’s continue to Raise The Standard in our education system together.

In His Service and At Your Service,

Ben Toews

Idaho State Senator – District 4

However, whichever, whenever government funding is given, applied, it always comes with strings attached, no matter what is said or promised. Think about it!

Thank you, Senator Toews